This exclusive data center report was prepared by ÈȵãºÚÁÏ Chief Economist, , and Associate Economist, .

Data Center Construction Starts Spending

ÈȵãºÚÁÏ reported that 22  broke ground in November 2025, with total starts spending exceeding $9.8 billion.

Project count declined slightly from 23 starts in November 2024, but the current month’s spending was nearly four times greater than the prior year’s total of $2.6 billion.

Initial November 2025 results indicate a year-to-date (YTD) total spending of $53.7 billion, representing a 138.6% increase over the same period in 2024.

Although ÈȵãºÚÁÏ has yet to finalize its December and full-year results, early indications suggest total 2025 spending will almost certainly exceed $60 billion.

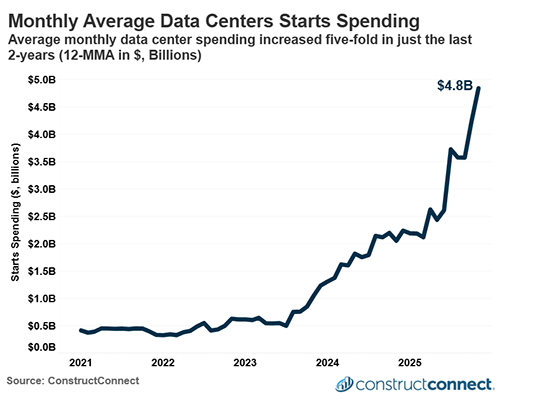

°Õ³ó±ðÌý sector’s expansion has been extraordinary from a long-term perspective as well. Assuming full-year 2025 starts of at least $60 billion, this would result in a 4-year compounded annual growth rate (CAGR) of 98%.

In short, this represents a doubling of starts every year since 2021.

Data Center Costs

Data center costs have surged over the past year on both a cost-per-center and basis.

In the 12 months through November 2025, the average data center cost was $597 million, with an average cost per square foot of $960. (Based on all projects with a square footage of more than 2,000 square feet).

For reference, the comparable results from a year ago were $374 million at $534 per square foot.

Although headlines have given great attention to dollar spending, the industry has actually trended toward slightly physically smaller centers over the past year, from an average size of 660,000 square feet a year ago to 623,000 square feet.

(Figures represent 12-month moving averages for all projects with a known square footage of over 2,000 square feet in size.)

Data Center Spending by Geography

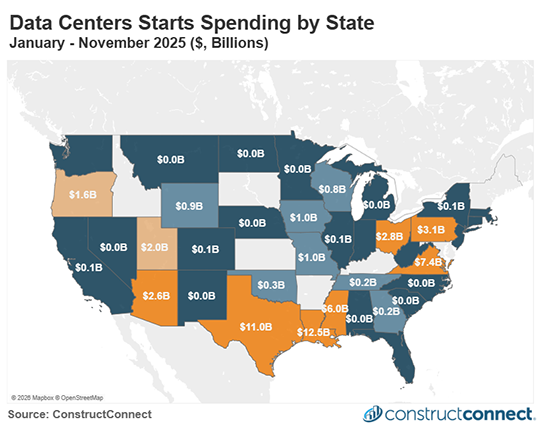

While data center projects have broken ground across most of the country year-to-date, the vast majority of investment has concentrated in just a handful of states.

The top 5 states for data center  YTD are Louisiana, Texas, Virginia, Mississippi, and Pennsylvania.

Together, these five states have seen nearly $40 billion in starts from January to November 2025, representing over 74% of total YTD data center spending.

Planned Data Center Starts for the Next 6 Months

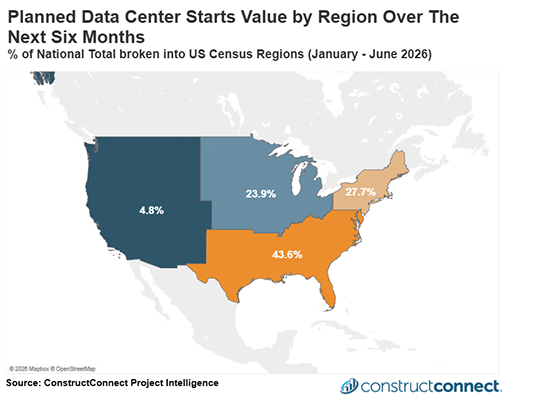

°ä´Ç²Ô²õ³Ù°ù³Ü³¦³Ù°ä´Ç²Ô²Ô±ð³¦³ÙÌý(CCPI) is tracking 65 Data Center projects, worth a total of $69.2 billion, that have potential start dates in the next six months. It is worth noting that these projects are in various stages of preconstruction with no guarantee of breaking ground.

Should a significant portion of these projects achieve their currently anticipated start dates, then 2026 starts spending will significantly outpace 2025’s record spending levels.Â

Based on ÈȵãºÚÁÏ’s Project Intelligence database of projects in , the trend of fewer but more expensive data centers is likely to persist.

Presently, ÈȵãºÚÁÏ is tracking 17 near-term megaprojects with values in excess of $1 billion, making up nearly 93% of the total project value for planned developments.

Additionally, geographic concentration remains evident among , with 80% of the potential starts spending occurring in just five states, including North Carolina, Pennsylvania, Texas, Virginia, and Illinois.

The limited number of high-value projects on the horizon also limits the level of participation among today’s . Given their tremendous size and complexity, data center opportunities are generally limited to only the largest and most capable construction firms.

This concentration limits opportunities for the broader construction industry, with many firms likely being excluded from participating in the boom despite massive headline investment figures.

Near-Term Energy Projects

Power infrastructure constraints represent a critical factor for continued data center expansion. ÈȵãºÚÁÏ projects  spending to reach $27.8 billion in 2026, rebounding from a lackluster 2025 reading of just $16.5 billion.

The pace of new power generation capacity will potentially restrain future data center development unless , including off-grid and privately developed power generation, can be found to quickly fill the expected gap between total power demand and the amount of power available to the public through government regulators.

Recent Comments

comments for this post are closed